.svg)

.svg)

July 16, 2026

The Digital Asset Operating Layer for Financial Institutions

Digital assets have become part of how modern financial platforms work — crypto deposits, institutional custody, tokenized assets, and bank-issued stablecoins are all on institutional roadmaps. But the infrastructure underneath is fragmented across wallets, exchanges, custodians, networks, and jurisdictions, and that fragmentation is what limits institutional scale. Digital asset infrastructure for banks is the operating layer that unifies those fragments — coordinating connectivity, identity verification, and routing and conversion through a single integration — inside the institution's own governance controls — so a financial institution can launch crypto capabilities without stitching the stack together itself. Mesh provides this operating layer through one integration serving multiple business units.

The practical question for a bank is no longer whether to support digital assets, but how to do it without accumulating technical debt, operational risk, and compliance complexity across a dozen point integrations. An operating layer answers that by making connectivity, verification, and orchestration a single coordinated capability rather than a series of one-off builds.

Not legal or compliance advice. This article describes capabilities and categories. Requirements vary by jurisdiction and institution; validate against your own compliance and legal review.

What is digital asset infrastructure for banks?

Digital asset infrastructure for banks is the coordinated set of functions — connectivity, identity verification, and routing and asset conversion, operating within the institution's own governance controls — that lets a regulated institution offer crypto and stablecoin capabilities to customers and across business units through one integration, rather than operating exchange, wallet, and chain infrastructure end to end. Delivered as an operating layer, it abstracts the fragmented external ecosystem into a single institutional interface.

It is best understood as a layer that sits between the institution's platforms and the external digital asset ecosystem: reaching where customers' assets already live, proving who controls them, moving them cleanly into institution-approved assets, and doing so within the institution's own policy and governance controls. It is also referred to as crypto infrastructure for banks or banking infrastructure for digital assets — an embedded crypto infrastructure, or crypto platform for financial institutions, delivered as a single integration.

Why does fragmented infrastructure hold banks back?

Because every wallet, exchange, network, and jurisdiction is a separate integration, and the complexity compounds across business units. As digital asset initiatives advance in parallel — one team on deposits, another on custody, another on settlement — each builds against its own set of external connections, with its own risk and compliance handling. The result is accumulating technical debt, elevated operational risk, duplicative integration overhead, and compliance complexity that grows faster than the capability it supports.

The demand reaching banks is concrete: customers increasingly hold digital assets on external platforms and want to bring them to the institutions they already trust — as deposits, as collateral, as managed assets. Every external balance a bank can't reach or verify is an asset that stays somewhere else. Serving that demand at scale requires coordination across platforms, rails, and assets — a unified connectivity and orchestration layer — not another point integration.

What does a digital asset operating layer do?

It coordinates four functions, spanning the path an asset takes from an external source into an institution:

Connectivity. Reaching customers' external wallets and exchange accounts through one integration. See bank-to-crypto connectivity.

Identity. Proving a customer controls the source — cryptographic user attestation for self-custody wallets, authenticated connection for exchange accounts — with an auditable link between wallet control and client identity. This is the basis of verified deposits.

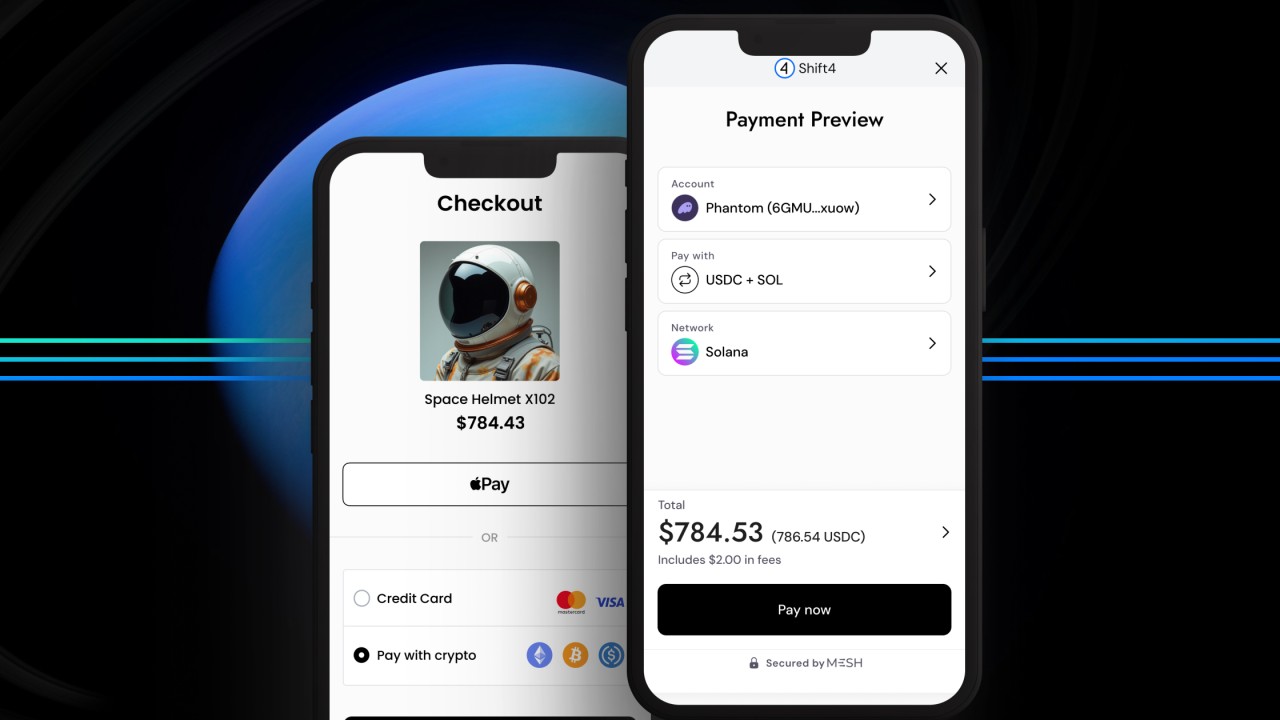

Routing and conversion. Coordinating the path from a connected source to the institution's destination and converting inbound assets into the institution's preferred assets. See account funding, powered by Mesh's engine, SmartFunding.

Governance stays with the institution. Policy definition, velocity and exposure limits, and risk parameters remain the institution's own — Mesh's functions operate inside that framework through configurable controls, rather than replacing it.

What can a bank do with it?

In practice, it delivers a few concrete capabilities:

- Global deposits — identity-linked digital asset transfers from external wallets and exchanges into the institution's platform.

- Asset conversion — inbound digital assets converted into institution-approved assets aligned with custody and risk frameworks.

- Integrity and compliance — wallet-control verification and structured audit trails supporting AML and regulatory requirements.

These are the live core for most institutions today.

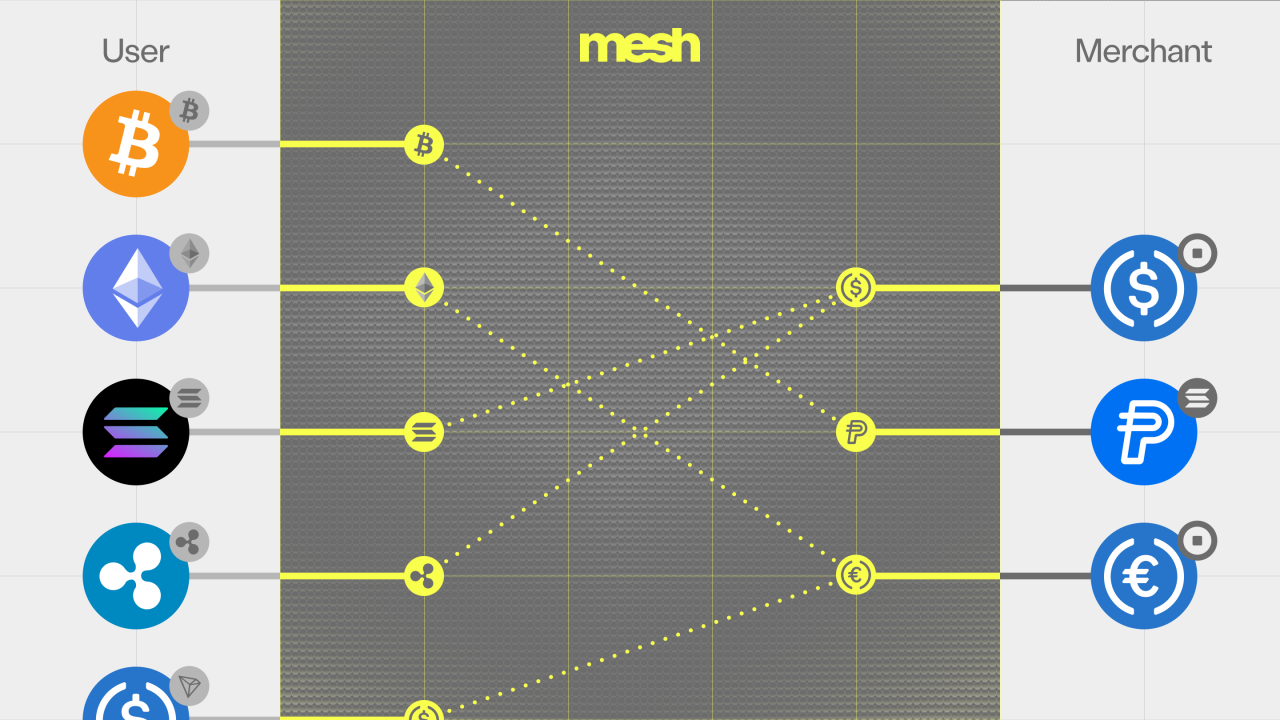

What does Mesh provide, and what does the institution retain?

This is the dividing line that keeps the model clean for a regulated institution.

Mesh provides connectivity across wallets, exchanges, and networks; verified identity linkage at the point of transfer; structured transfer metadata and blockchain risk signals; and configurable transaction parameters.

The institution retains policy definition and enforcement; velocity and exposure limits; custody, quarantine, and recovery authority; and AML case management and regulatory reporting.

In other words, Mesh coordinates connection, verification, and movement at the infrastructure layer, and leaves custody where the institution wants it: the bank holds assets itself or with its chosen custodian. Because custody stays the institution's choice, adopting the operating layer doesn't force a change to how the bank holds assets.

How fast can a bank go live?

Weeks, not quarters. Because the operating layer replaces many point integrations with one, an institution moves to production via modular API/SDK integration rather than a multi-quarter build, and the burden of keeping pace with each platform's protocol, connectivity, and compliance changes shifts to the layer rather than the bank's engineering backlog.

Who is already using this approach?

AMINA Bank, the Swiss FINMA-regulated crypto bank, integrated Mesh for verified deposits — embedding connectivity, verification, and funding directly into its online banking platform.

Paxos, the regulated blockchain-infrastructure and tokenization platform, integrated Mesh so the institutions it serves can offer verified connectivity and funding from external sources to their own customers, including for assets such as PYUSD and USDG.

Frequently asked questions

→ What is digital asset infrastructure for banks? The operating layer — connectivity, identity verification, and routing and conversion, operating within the institution's own governance controls — that lets a bank offer crypto and stablecoin capabilities through one integration instead of building the stack in-house.

→ What is a digital asset operating layer? A single coordination layer that unifies fragmented external infrastructure (wallets, exchanges, networks) into one institutional integration, so multiple business units share the same connectivity, verification, and orchestration.

→ What can a bank launch first? Typically global (verified) deposits and connectivity — accepting and verifying customer funding — followed by asset conversion as the institution's digital asset activity matures.

→ How long does integration take? Weeks rather than quarters, via modular API/SDK, because one integration replaces many and maintenance shifts to the operating layer.

→ What regulations apply? It depends on jurisdiction and activity — EU MiCA and the Travel Rule (Transfer of Funds Regulation) in Europe, Bank Secrecy Act obligations in the US, and others. Confirm with your compliance/legal team.

Related reading

- Verified Deposits: Wallet Ownership Verification for Banks

- Bank-to-Crypto Connectivity

- Account Funding for Banks

- How SmartFunding Orchestrates Any-to-Any Funding

- Mesh for Banking

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20(1).png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)